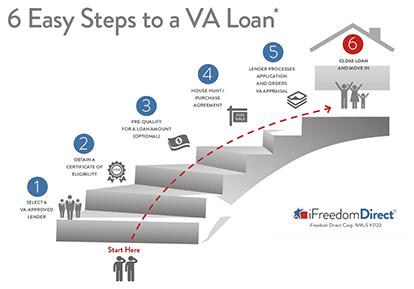

For many borrowers, applying for any kind of mortgage may seem daunting. But, when broken down, this rundown of 6 steps to getting a VA loan is easy to understand.

1. Select a VA-approved Lender

On the surface, it might appear that any lender will do. However, if you dig a little deeper, you may discover that not all lenders are the same. First, only lenders approved by the U.S. Department of Veterans Affairs can originate VA mortgages. Secondly, some lenders focus primarily on conventional loans, while others concentrate almost exclusively on the VA loan program for military clients. Using a VA specialty lender with extensive knowledge about the VA loan process vs. a lender who only funds a few VA mortgages a year may translate into an easier and quicker loan process. To connect with a VA specialty lender and compare options from the top VA loan lenders, please click here.

2. Obtain a Certificate of Eligibility (COE)

An experienced lender can help you obtain what’s called a Certificate of Eligibility (COE). The COE will prove that you meet initial eligibility standards for VA loan benefits. It will also let the lender know how much entitlement you can receive, which is the amount the Department of Veterans Affairs will guarantee on your VA loan. To get your COE, you’ll need to give your lender a bit of information about your military service. Usually, a COE can be acquired online instantly through a lender’s portal or through the eBenefits portal on the va.gov website. Those servicemembers or surviving spouses whose COEs cannot be obtained online will have to get theirs by mail. A VA lender or the VA can help direct you to the right resource for your specific situation.

3. Pre-Qualify for Your Loan Amount (optional)

Pre-qualifying is important, but not required. By choosing to complete this step you can save some time and potential surprises later in the process. To pre-qualify for your loan amount, you’ll have a candid conversation with your VA loan professional about your income, credit history, employment, marital status and other factors. Giving your lender complete details during the pre-qualifying step can help prevent surprises later during underwriting. The pre-qualifying step can also reveal areas that need improvement before you can be approved, such as credit or debt-to-income ratio. While a prequalification letter gives you a ballpark price range for house hunting, it does not guarantee that you will be approved for a loan, and your lender will later have to verify the information you provide. To get a loan requires later final approval by underwriting once all documents have been received and reviewed (see Step 5).

4. Go House Hunting and Sign a Purchase Agreement

The fourth step is usually one borrowers enjoy because they get to look at homes they might consider buying. Working with a real estate professional who specializes in the VA process can help you get the most out of your benefits. This is true because the VA allows certain fees and costs to be paid by the seller (if both you and the seller agree), and a knowledgeable agent will know this and help you negotiate seller-paid fees. Once you’ve got a signed purchase agreement, you can move forward in the VA loan process.

5. Lender Processes Application and Orders VA Appraisal

A signed purchase contract is the document you’ll need to finish your initial application. Once your lender has the contract, they will order the VA appraisal. Here again, not just any appraiser will do. Only a professional who is certified to perform appraisals to VA standards can evaluate the home being considered for VA financing. The VA appraiser will make sure the price you’ve agreed to pay for the home corresponds with the current value. Another very important part of the VA appraisal is to inspect the home to make sure it meets the VA minimum property requirements (VA MPRs). However, the VA appraisal does not take the place of a home inspection, which focuses on code violations, defects and the condition of the property. While many borrowers have heard horror stories about the length of the VA appraisal process, the Department of Veterans Affairs gives the appraisers 10 days from order to completion barring extenuating circumstances. While you’re waiting for appraisal documents, you’ll be busy submitting documents of your own to your VA-approved lender to show you have the ability to qualify for the loan. If the home passes appraisal for value and VA minimum property requirements, and it’s verified by the lender that you qualify for your loan, the underwriter will give his or her stamp of approval.

6. Close on Your Loan and Move In

After being approved by the underwriter, all that is left to do is close and move in. During closing, the property legally transfers from the former owner to you. Closing is a step that requires you to sign documents that confirm you understand and agree to the terms of the loan. You will need to provide proof of homeowners insurance and, if required, pay closing costs. After closing, many homeowners later explore options such as rate reductions or cash-out opportunities by learning how to refinance a VA loan.

While these steps may not happen in the order above or be a required part (such as prequalification)*, they represent the typical process for the applicant in obtaining a VA purchase loan. Your lender may need to take other steps. For more information about VA loans, contact an experienced VA-approved lender.

Ready to Get Started?

If you're ready to get started, or just want to get more information on the process, the first step is to connect with a preferred VA Loan lender. You can then discuss qualifications, debt to income ratios, and any other concerns you have about the process with the lenders.

")

")

")

")