Having credit card debt can cost you more than you think. Yes, obviously you pay interest on that debt. But it can cost you in more hidden ways as well.

Listen my child, a little bit more

And I’ll tell you about your credit score

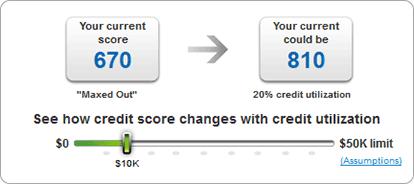

Thirty percent of your credit score is determined by your credit utilization, which is the ratio of your outstanding balances on all revolving credit (usually credit cards and home equity lines of credit) compared to the credit limits on those accounts. If you have a balance of $2,000 on a credit card with a $5,000 limit, your utilization rate is 40%.

How utilization is your utilization rate used?

Your utilization rate is used two ways in calculating your score—on aggregate (the sum of all your balances divided by your total credit limits) and individually (the same ratio for each individual card). Credit analysts have determined that the higher balance you have relative to your credit limit, the more likely it is that you default on your loan. This is reflected in a lower credit score.

What should utilization rate be?

An ideal credit utilization rate would be less than 10% on individual accounts and overall, although less than 20% is still pretty good. Once your credit utilization rate goes over 40%, your credit score will be very significantly impacted. Depending on your starting point, the difference between 10% utilization and 100% utilization can be nearly 100 points.

How much does this cost?

The impact of high utilization comes primarily through a lower credit score which will raise your interest rates. For example, if you have a 650 credit score, your credit card rates are most likely around 18%. If your credit score were 760 or above, your interest rate would likely be only around 8%. That’s a difference of $1000 per year in interest for every $10K you carry in balance. And that same difference in utilization can add nearly 1% to your mortgage interest rate, costing you tens of thousands of dollars over the lifetime of your mortgage.

See a sample calculator here:

http://www.savvymoney.com/creditscoresavings

How can I reduce my utilization rate?

There are two ways to reduce your utilization—add more limit by taking out additional credit or by paying off existing balances. Opening more accounts tends not to work very well—first, your credit score will take a hit from the additional inquiries when you open an account and second, despite best intentions, that open balance tends to get spent, leaving the borrower even worse off. Our recommendation is to improve your credit score by paying off balances and targeting a credit utilization rate of less than 20%.

")