Kate's note: I've recently had a lot of questions about Social Security benefits for spouses who didn't work, or worked significantly less than their husband or wife. It's an important issue, so I reached out to my friend and Social Security expert Devin Carroll to give us an overview. Devin is a financial planner, author of the Social Security Intelligence blog, and co-host of the Big Picture Retirement podcast. He's my go-to resource for Social Security questions! This post is a re-write of a post at the Social Security Intelligence blog.

Most couples have one partner who has been the primary wage earner. It’s hard to raise a family with two full-time careers! When planning for retirement, it’s important to know about the spousal benefits provided by America’s Social Security program. Social Security currently makes up an important part of most family's retirement income plan. Understanding your entitlements is an important part of planning.

A recent Social Security report found that 2.3 million individuals received at least part of their benefit as a spouse of an entitled worker. Some of these spouses had benefits of their own, but were eligible to receive higher benefit because the spousal benefit amount was greater than their own benefit. Some of these individuals have never worked outside the home or paid Social Security tax. They have no benefit of their own and rely exclusively on the Social Security spousal benefit available under their spouse’s work record.

And it’s not just retirement income benefits. Eligible spouses also receive premium free Medicare benefits.

Let’s take a look at what it takes to qualify as well as what benefits you may receive as an eligible spouse.

(If you don’t have a basic understanding of how Social Security works, you may want to first watch this short video: Social Security Basics.)

What Does it Take to Qualify?

Unlike most rules related to Social Security, the rules for the spousal benefit entitlement are pretty easy.

If you’ve been married to your current spouse for at least one year, you’re eligible for a spousal benefit under their work record. However, there are two big exceptions to this rule:

- If you marry someone that is the natural mother or father of your child, the one year requirement is waived.

- The one year requirement is also waived if you were entitled (or potentially entitled!) to Social Security benefits on someone else’s work record in the month before you were married. An example of these benefits would be spousal benefits, survivor benefits or parent’s benefits. For example, let’s assume you will be eligible for a spousal benefit from your ex-husband Joe. If you remarry, you wouldn’t have to wait the full 12 months to get a spousal benefit from your new spouse. Instead, you’d be immediately eligible.

If you’re divorced, and not currently married, you’re eligible for a spousal benefit if the marriage lasted for at least 10 years.

How Much is the Spousal Benefit?

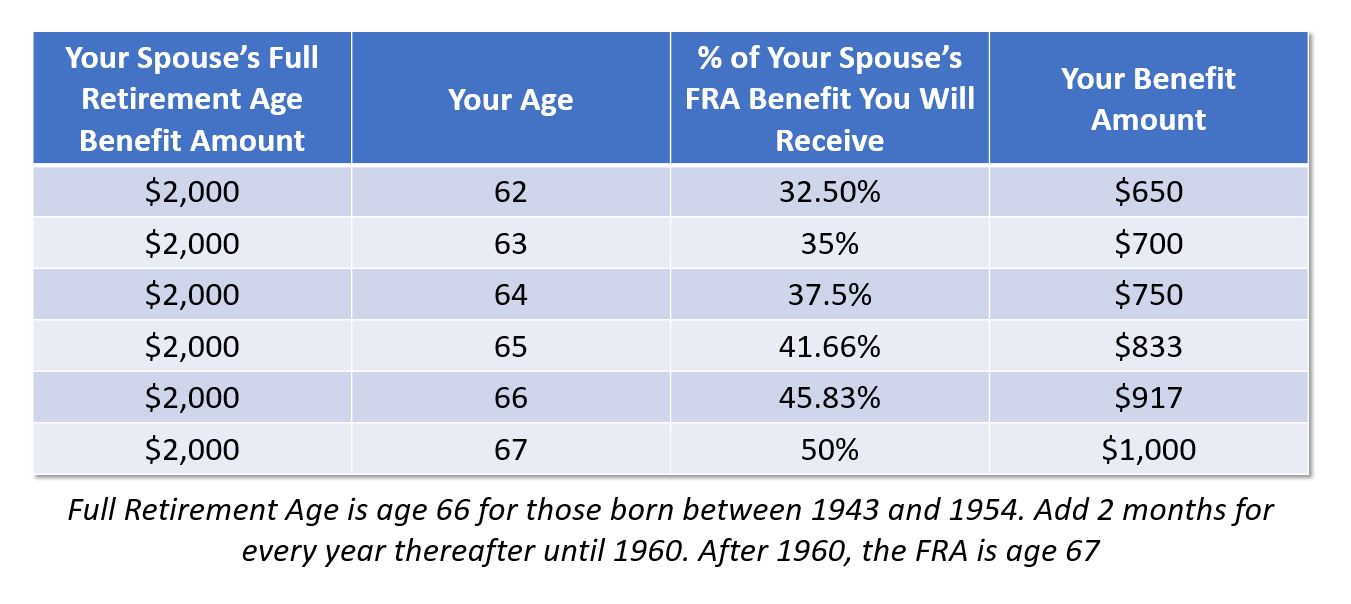

The spousal benefit can be as much as 50% of the higher-earning spouse’s full retirement age benefit. For example, if your spouse has a full retirement age benefit amount of $2,000, your spousal benefit amount at your full retirement age would be $1,000.

It’s important to note that this benefit can never be more than 50% of the higher-earning spouse’s full retirement benefit, but it can be less! Why? It’s based on your filing age. Depending on how old you are when you file, the spousal benefit amount will range between 32.5% and 50% of the higher-earning spouse’s full retirement benefit.

In the chart below we’ll assume that your full retirement age is 67. We’ll further assume that your spouse’s full retirement age benefit is $2,000 per month.

You probably noticed the steep penalty for filing early. You may have also noticed that the spousal benefit does not increase beyond your full retirement age. So if a spousal benefit is all that you are entitled to, as we assume in the chart above, there is usually not a good reason to delay filing beyond your personal full retirement age.

How Spousal Benefits are Calculated (the right way)

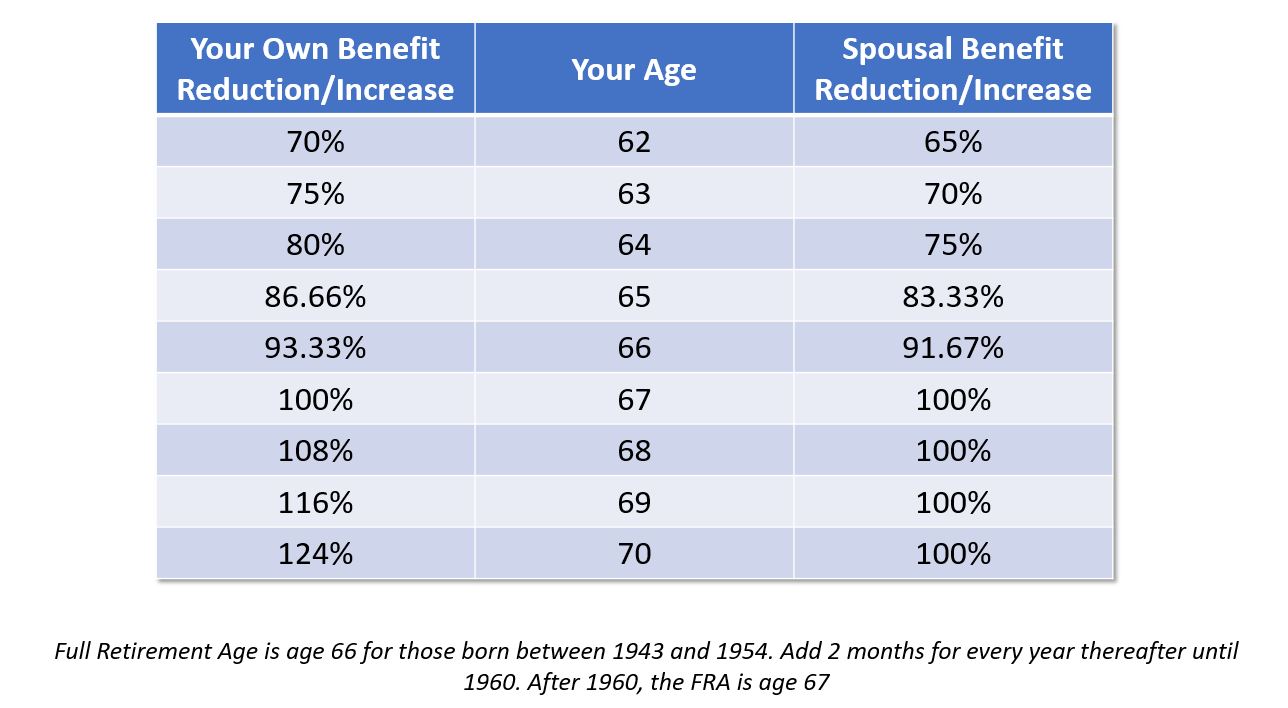

The spousal benefit calculation is straightforward if you don’t have a benefit on your own. However, it can seem a little more complicated if you have Social Security benefits from your own work history. To keep things interesting, the SSA decided that a different calculation method should be used to determine how much each benefit should increase/decrease based on your filing age.

I’ve made a video that goes over this calculation step-by-step. Check it out! VIDEO: How To Calculate Spousal Benefits The RIGHT Way

Thankfully, if you understand how they break down the individual benefits, it’s not hard to use the table above to quickly figure out what your approximate benefit will be. Here’s an example.

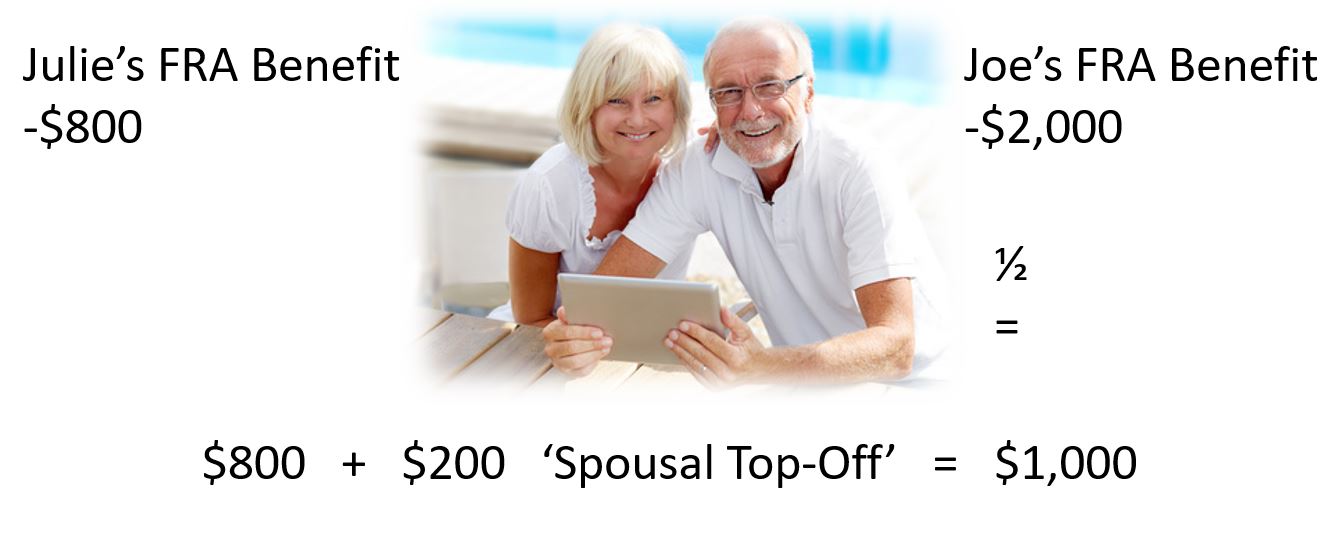

Joe and Julie each have a Social Security benefit from work they individually performed. Julie’s benefit at her full retirement age is $800 per month. Joe’s benefit at his full retirement age is $2,000. Assuming they are both full retirement age when they file, Joe will be entitled to a benefit of $2,000 and Julie will be entitled to the great of her own benefit or half of Joe’s benefit. Since half of his is greater than hers ($1,000 vs. $800), she will receive $1,000.

Sounds simple, right?

In this scenario, it really is simple. But when it comes to calculating different age combinations, it’s really crucial to understand that Julie will always receive her own benefit amount first and then receive a “spousal top-off” to get her benefit to 1/2 of Joe’s. It’s those two benefits that are subject to different calculation with regard to how they are increased or decreased based on filing age.

For example, if Julie filed at 62 her $800 benefit would be reduced to $560. The $200 ‘spousal top-off’ would be reduced from $200 to $130. In this scenario her combined benefit would be $690.

It’s important to note that the ‘spousal top-off’ is only available once the higher earning spouse files for his/her own benefit. This means that if Julie files for her own benefit, but Joe does not, Julie would only be entitled to the benefit on her own work record. Once Joe filed, she would begin receiving the additional spousal top-off benefit.

It’s also important for planning to understand that the spousal benefit would be reduced (or not) based on age of entitlement to that benefit. This means that Judy’s reduction to her own benefit would be based on her age when she filed for her benefit. However, her reduction to the spousal benefit would be based on her age when Joe filed for his benefit.

So, if Judy filed when she was 62, her own benefit would be reduced. If she was 67 when Joe finally got around to filing, her spousal top-off would not be reduced.

Significant Rule Exception If You Are Divorced

When planning your Social Security filing strategy, it’s important to note that you cannot file for a spousal benefit until the higher earning spouse files for their benefit. However, this does not apply if your are filing for a spousal benefit from an ex-spouse. If your ex-spouse has not applied for retirement benefits, you can receive benefits on his or her record if you have been divorced for at least two years.

Medicare Coverage

If you are eligible for a Social Security spousal benefit, you are also entitled to premium free part A Medicare at age 65…but only if your spouse is at least 62 years old.

If you are more than 3 years older than your spouse, you may have to buy Medicare Part A until your spouse turns 62. That’s when your premium-free benefit would start. The Part A monthly premium is $413 in 2017.

Parting Thought

As a parting thought, it’s important that you get this benefit right the first time. If you file early, you generally don’t get to go back and make changes. Take the time to understand the benefit thoroughly before filing!

Further reading: Closely related to the Spousal Benefit is the Social Security Survivor Benefit. I’ve written an in-depth, but easy to understand, article titled Social Security Survivor Benefits: The Complete Guide to Who Gets What and How to Calculate It

")

")

")

")

")

")

")