It's a tale as old as time. You show up to work on Monday morning and see an unfamiliar vehicle parked out front -- probably an old V6 Camaro with bald tires and fresh drops of oil on the pavement. A few moments later, you encounter a young service member with an ear-to-ear smile and a credit score of "never heard of you." The senior noncommissioned officer and officer in charge are rubbing their temples to ease the ensuing migraines. The used-car dealership outside the front gate has struck again.

Everybody appreciates a nice car, especially if you're a young service member with real money in your pockets for the first time. The barracks provides housing, the chow hall feeds you, and Tricare doesn't charge a dime -- those bimonthly paychecks have to go somewhere, right? Might as well treat yourself to a hot set of wheels.

Except the wheels are rarely as hot as you think they are, and the financial repercussions can be disastrous. The Kelley Blue Book price comparison the salesman provided was for a Camaro 1SS, but the car on the lot was a Camaro 1LT with a starting MSRP that's more than $10,000 lower. The maintenance history? Nonexistent. The financial terms? Appalling.

Seeing shady car dealerships take advantage of young service members turns my stomach. It happens way too often and the fix is easy, we just have to share information and help people make smart financial decisions. This is everything you need to know about why high-APR interest rates are a problem, how much they can cost you in the long run, and where you can find a loan that works for you – not against you.

"I Got 30% APR. Is That Bad?"

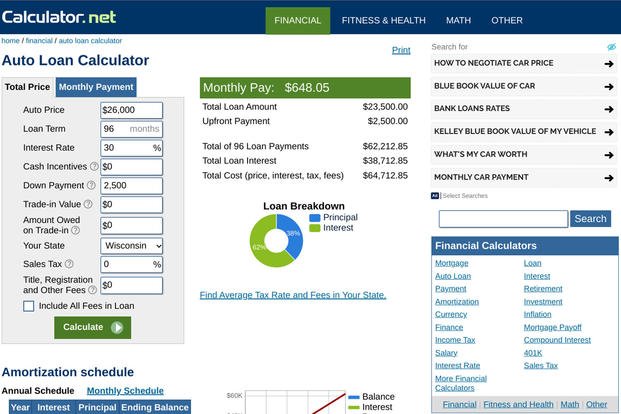

According to Kelley Blue Book, the average used car cost $26,091 as of November 2023. We'll use a hypothetical purchase price of $26,000 to run some quick numbers, and we'll use the Auto Loan Calculator to do some math for us, ignoring state-specific taxes and fees.

Let's say you put down $2,500 when you buy the car (roughly a month's pay for an active-duty E-3 with more than two years of service, according to the 2024 military pay charts). That leaves $23,500 to finance. The dealership isn't going to let you spread payments over several years out of kindness, so they're going to charge interest, otherwise known as the annual percentage rate. That's where the dreaded 30% APR that's starred in so many weekend safety briefs comes into play.

The sales staff might give you what sounds like good news: It can get your monthly payment down to $648 per month, which is only about a quarter of your monthly base pay. Great! What they don't mention is that achieving that payment amount necessitates stretching your 30% interest loan period to 96 months (which is a thing people are doing now).

You'll spend eight years paying for your $26,000 used car, whether it lasts that long or not. Over that period, 38% of your money will go toward the car and 62% will go toward interest on the loan. This contract will ultimately cost you $62,213 in combined principal and interest.

That's all very terrible, but it gets much worse. The average American is keeping their car longer than ever, according to PBS, but if you want to trade in your car for something else, you'll be in trouble. Let's say that after three years, you start a family or just want something different. You've got 36 payments of $648 under your belt, so the car must be nearly paid off, right? Not even close.

Because the interest on auto loans is front-loaded, most of your money goes into the lender's pocket rather than the equity in your car at the beginning of the loan term. In this scenario, you would still owe $20,030 on your $23,500 loan after paying $23,330 into it. When you trade in your vehicle, you'll have to factor the $20,030 debt into the price of your next car.

This holds true if you lose your car to an accident. Even if your insurance company issues a payout, that amount is based on the insured value of the car, not what you owe on it. If you owe more than it's worth, you'll still owe the balance to your lender. Does your soul hurt yet?

Here's What Most People Actually Pay

According to Experian, the average loan term for used-car buyers in 2023 was 68 months. The average interest rate for this kind of loan was 11.97%.

Based on those numbers, the total amount of money you would spend on the same $26,000 car with a $2,500 down payment is $32,477. After three years, you'd only owe $13,029. That's not wonderful, but it's far more manageable than our last example.

When more savvy service members fly into a fit of rage over high-interest auto loans, this is why. There are much better ways to buy a car than with the stereotypical 30% APR. Even the national average is a vastly more desirable alternative.

Auto Loans that Work on Your Behalf

Your search for a favorable auto loan should begin long before you set foot on a dealership lot. Securing financing outside of the dealership can yield a better interest rate and create more room for you to negotiate with a seller on price.

Some lenders offer special interest rates or incentives for service members and their families. Navy Federal Credit Union offers rates as low as 5.44% for 36 months on used vehicles. Active-duty and retired service members can reduce their rate by 0.25% through NFCU's military discount.

Individual interest rates are determined by several factors, but you can get a good idea of what your options are with NFCU's auto loan calculator.

The Department of Veterans Affairs doesn't offer auto loans, but it has a helpful guide to banks and credit unions that are good options for the military community. According to this guide from the VA:

- Bank of America offers excellent loans for people with very good or exceptional credit.

- Armed Forces Bank makes securing credit relatively easy.

- USAA offers extremely competitive rates in addition to a 0.25% rate discount for setting up automatic payments (which you should be doing anyway).

- Chase Bank typically offers competitive rates on three- to five-year auto loans for people with good or excellent credit.

- Pentagon Federal Credit Union offers excellent rates on auto loans from $500 to $100,000.

- Navy Federal Credit Union offers flexible lending options and competitive rates on cars, motorcycles, RVs and boats.

- Service Credit Union offers some of the lowest rates in the industry.

Not sure if your credit score is good or bad? Experian has a guide to help you understand what you're working with.

If you assumed any kind of debt prior to joining the military, brush up on the Servicemembers' Civil Relief Act (SCRA) to make sure you aren't paying more in interest than you need to. Unfortunately, this legislation can't help with debt you take on while serving in the military.

Auto Manufacturers with a Military Discount

One of the best ways to minimize your auto debt is to reduce the price. Margins on used cars tend to be very tight and leave dealerships without much wiggle room, but some manufacturers offer military discounts on new vehicles. New cars obviously cost more than used ones, but interest rates are lower for new vehicles so it's worth shopping around.

Most auto manufacturers that do business in the U.S. offer some form of military incentive, be it a discount, maintenance program or overseas purchasing assistance. Check our list of current auto discounts to see what each brand is willing to do to earn your business.

Finding the Right Car Matters, Too

Financing aside, you should only spend money on a car that you know is in good shape. If it's not completely up to spec, you should at least know what needs to be fixed and how much the repairs will cost.

A pre-purchase inspection is always a good investment and asking for one is totally within your rights as a customer. For example, if you're buying a Honda from a generic used-car lot or private seller, arrange to have the car checked over by a technician at your local Honda dealership who knows what they're looking at.

Expect to pay for one hour of labor for a pre-purchase inspection, or PPI. Afterward, the service department will provide a list of all the issues it found and an estimate for what it would charge to fix them. You can take that back to the seller when you negotiate or budget to pay for the repairs yourself.

Some issues, like deferred maintenance, can't be detected without comprehensive service records. The inspecting tech may have questions like, "Did the previous owner replace the timing chain tensioners at 60,000 miles?" If there are no records of these maintenance items, plan on having them addressed as soon as possible.

The Bottom Line

Too many used-car dealerships prey on young service members who have a reliable income, limited financial literacy and orders that will take them far away before they can realize what they've gotten themselves into and warn other service members. My advice has always been the same: If you walk into a dealership and they greet you by your branch of service ("Hey, soldier!"), run.

Most car dealerships do business the right way, but they generally aren't the ones slinging used cars they bought at auction across the street from a military installation. Be your own biggest advocate. Talk to your chain of command, research the car-buying process online and get as much high-quality financial advice as you can. Remember, nobody is committing to monthly payments but you.

If you play your cards right, you can have a car that adds value -- not stress -- to your life.

Want to Know More About the Military?

Be sure to get the latest news about the U.S. military, as well as critical info about how to join and all the benefits of service. Subscribe to Military.com and receive customized updates delivered straight to your inbox.