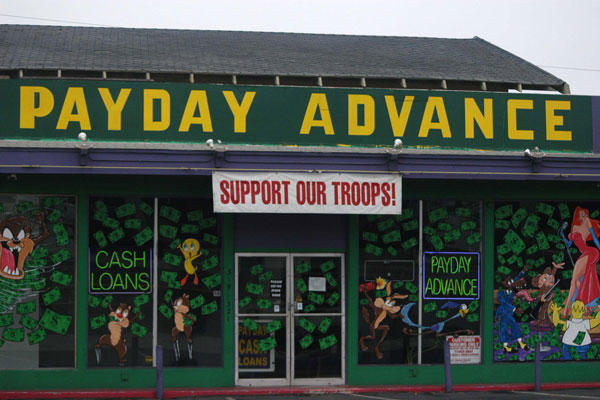

The payday loan institutions that operate outside military bases have found loopholes in existing law and created new lending scams to prey on servicemembers, federal and state regulators warned Congress last week.

"There are scoundrels out there and they have to be uncovered," Sen. Jay Rockefeller, D-W.Va., chairman of the Senate Commerce Committee, said Thursday at a hearing on predatory lending practices aimed at the military.

Young servicemembers make appealing targets for "unscrupulous" businessmen who hide interest rates that can exceed 300 percent in the fine print and threaten to disclose the debts to commanders to exact payment, Rockefeller said.

In an effort to crack down on predatory lending, Congress in 2006 passed the Military Lending Act that capped interest rates at 36 percent, but "lenders have easily found ways to get outside of the definitions," said Holly Petraeus, head of the Office of Servicemembers Affairs at the Consumer Financial Protection Bureau.

"I've lived on or near military bases my entire life, and seen that strip outside the gates, offering everything from furniture to used cars to electronics to jewelry, and the high-cost credit to pay for them," said Petraeus, noting that payday lenders congregate outside bases "like bears on a trout stream."

Short-term loans not covered under the 36 percent rate cap include loans for more than $2,000, loans that last for more than 91 days, and auto-title loans with terms longer than 181 days, said Petraeus, the wife of retired Army Gen. David Petraeus.

Fast-talking lenders have also targeted servicemembers seeking home mortgage financing, "falsely implying that the loans are from the VA [Department of Veterans Affairs]" and using agents who pass themselves off as official military liaisons, said Charles Harwood, deputy director of the Federal Trade Commission's Bureau of Protection.

In one instance, the FTC was able to hit a lender with a $7.5 million civil penalty for running a scheme involving supposedly low-interest, fixed-rate mortgages, Harwood said.

The payday lenders have also focused on the military allotment system to get around the law, Harwood and Petraeus testified.

The lender will have the servicemember complete the loan application online, and the loan repayment and finance charges are then electronically withdrawn on the servicemember's next payday, Harwood and Petraeus said.

The result was that certain lenders now look upon servicemembers as a "money delivery system" for their fraudulent deals, said Dwain Alexander, a legal assistance officer for the Navy's Mid-Atlantic Region.

Despite the current law, the volume of payday lending for both civilians and servicemembers has grown exponentially nationwide. A study by the investment bank Stephens Inc. showed that payday lending on short-term loans at high interest rates grew to $18.6 billion in 2012, up 10 percent from the previous year, according to The Wall Street Journal.

At the Senate hearing, Tennessee Attorney General Robert Cooper testified that scams run by Rome Finance LLC and Britlee Inc. ensnared more than 4,000 soldiers from Fort Campbell, Ky., with high interest rates and markups for laptops and other electronic devices.

Many of the victims were young troops about to deploy to Iraq or Afghanistan who wanted the devices to communicate with their families, Cooper said. One family was hounded by bill collectors for debts incurred by a soldier killed in Baghdad, Cooper said.

The Tennessee Attorney General's office was able to win more than $2.2 million in civil penalties against Rome Finance and Britlee, and put them out of business in Tennessee.

However, those same companies simply moved to New York and set up shop outside Fort Drum, home of the Army's 10th Mountain Division, near Watertown, N.Y., said Janet Nelson, head of the regional office of the N.Y. State Attorney General's office.

Britlee and Rome now operate under the name SmartBuy from a shopping mall near the base, and run the same scams on electronic devices, Nelson said. Soldiers began complaining to her office that "they didn't know why the computer wasn't paid off yet," Nelson said.

In one case, a soldier who bought a PlayStation 3 and 32-inch Vizio TV for $162 a month was never told the total cost would be $3,123 plus interest, the N.Y. Attorney General's office said.

In 2012, the N.Y. Attorney General's office won settlements of $12.9 million against SmartBuy and its affiliated companies and began refunding soldiers who were defrauded.

At the Senate hearing, lawmakers from both parties said they were looking at closing loopholes in the current law that allow predatory lending practices to continue, but they also said that the only long-term solution rested with a combination of better law enforcement and improved consumer education for the troops.

")

")

.")

")

")

")

")

")

")

")

")

")

")

")

during an evacuation at Hamid Karzai International Airport, Kabul, Afghanistan, Aug. 21, 2021 (U.S. Marine Corps photo by Staff Sgt. Victor Mancilla)")

")